Even as cable/satellite TV carriers like Comcast and DirecTV squabble over dollars and cents with broadcast and cable networks like NBC and Viacom, the very structure of their decades-old business model is under attack from new Internet technologies and services, as well as new government regulations. At stake is the future of how people watch and pay for television and video – and who controls the experience.

With plot twists like last-minute negotiations ending in content blackouts, regulatory changes that could derail well-established business models, and brand new technologies delivering video content in brand new ways, this TV-delivery drama should be a blockbuster.

The question is, what surprises will the next episode bring? The search for possible spoilers brings up a wide range of theories from all over the industry, as various players, regulators and observers try to figure out what happens next.

Kevin Lockett, Digital Media Analyst from Lockett Media, says the result will be a fundamentally changed cable industry – one that will have to be far more transparent and flexible in order to keep its customers from defecting to new Internet-based options. If and when the general public figures out that it now has real alternatives, Locket says, “the cable companies are in trouble.”

Previously On Cable TV…

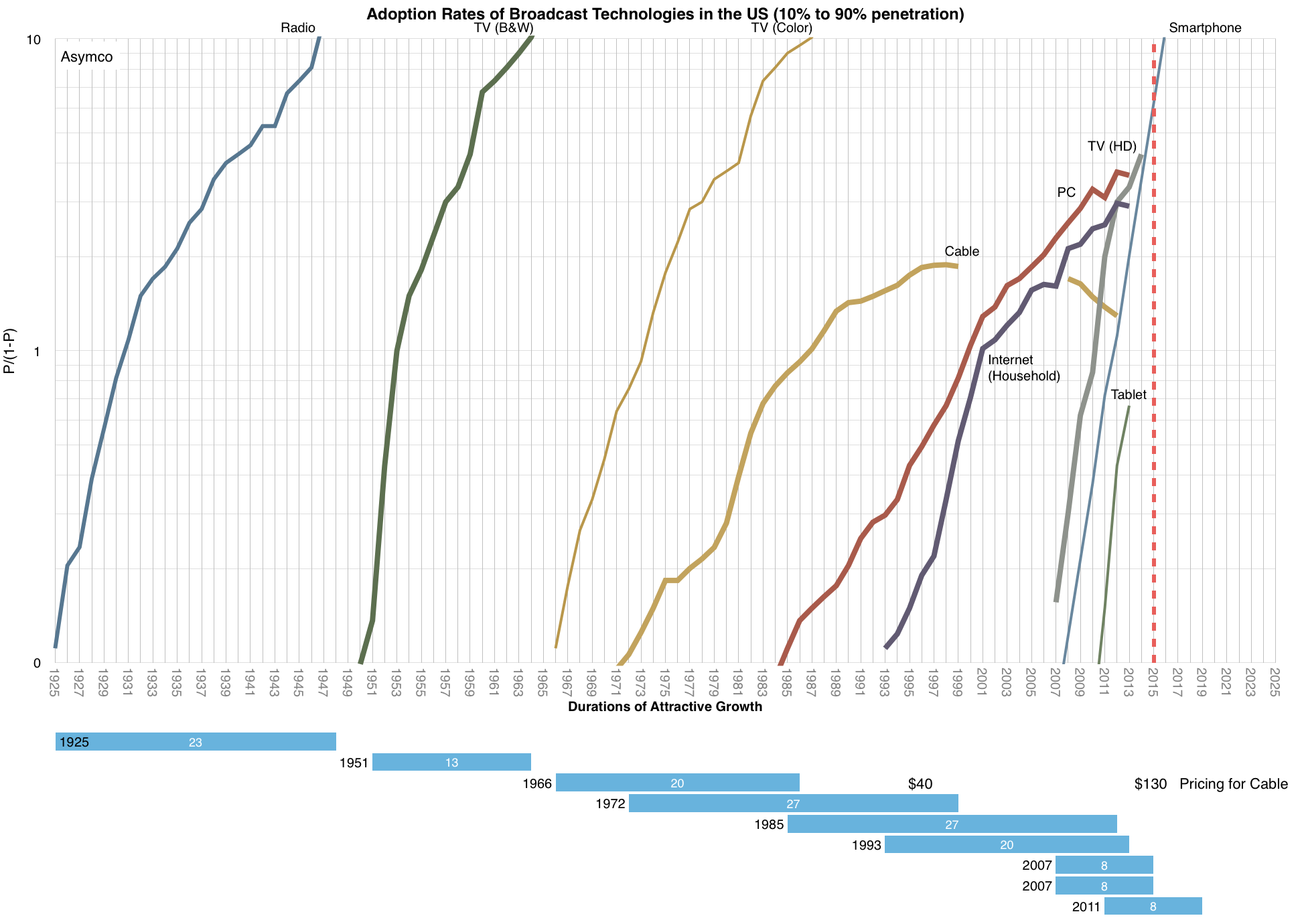

For two decades, cable TV, joined later by satellite providers, has been the dominant force in delivering video content to homes and businesses in the US. Lately that dominance has been challenged from within by cable TV’s own business practices and from without by Internet video providers like YouTube and streaming Internet TV delivered to special set-top boxes with weird names like Roku and Boxee, or Blu-Ray DVD players, or even “Smart” TVs themselves.

This new class of technology is hard to label, since there are so many variations on delivery devices, but over the top (OTT) platforms is one name that seems to be getting some traction. OTT is a broad term that describes not only the devices that receive and display Internet TV, but also the online services that deliver them. A tablet, then, is not an OTT device in itself, but it can receive OTT-delivered content, such as that from Hulu and iTunes.

OTT devices vary in form, but they share the function of bringing in video content over existing Internet connections through service providers like Hulu, Amazon Instant Video, and Netflix. Such services feature on-demand video programming at monthly rates that are typically much lower than cable subscription rates (for a more limited range of content, of course).

Who’s Gone Over The Top (OTT)?

How much attention is OTT getting? The Interpret LLC’s New Media Measure syndicated report sets the number of US consumers age 18-65 that own an Internet-enabled set top box (like a Roku player, Apple TV, Slingbox, Vudu box, etc.) at 13.6%, reported a company spokesperson.

Less than 14% may not sound like much, but OTT has been around for only three years. And Interpret’s numbers don’t include the millions of users watching alternate video sources like YouTube and Vimeo.

The other half of the squeeze on the cable TV industry comes from the ossified business practices of the industry itself. Cliffhanger battles for carriage rights that lead content creators to pull their programming from cable and satellite systems if they can’t get a deal they like is shooting the industry in the foot.

Frustrated with what appear to be more frequent content blackouts and ever-rising rates, consumers – and lawmakers – are applying pressure for less bundled programming and more à la carte-style programming. Content providers like Viacom and Disney rely on channel bundles to keep alive channels that consumers might not otherwise pay for.

Bundling Is The New Villain

The animosity over channel bundling is building. During the recent dispute with Viacom that led to a content blackout of Viacom channels for 26 million viewers, DirecTV laid it all out for the New York Times:

“Programmers like Viacom typically won’t allow anyone to buy their channels individually, but we hope to change that,” DirecTV told the Times. “We currently pay them hundreds of millions of dollars every year already, and if Viacom thinks their networks are worth a billion more, then you have to be able to select what’s most important in your own living room.”

DirecTV was willing to endure public blowback for dropping popular Viacom channels lilke Comedy Central and Nickelodeon because it was more afraid of bundling. In the past, customers had little choice but to pay for channels they didn’t watch to get the ones they were interested in.

But things are changing. Now customers can go to competing cable companies in the same town, or buy a satellite dish. Or leave the game completely to use OTT devices and services. Suddenly, the cable companies are pushing back at bundling demands from content producers.

Finding the Plot Motivation

As vice president of Accedo, a software vendor that builds apps and application interfaces for OTT devices, David Adams knows first hand about the changes in the cable TV industry.

“We’ve moved from just a few services in there with their toes in the water, to these services actually driving strategy,” Adams explains.

Ironically, though, the barriers to sweeping change within the existing cable TV industry are the same factors driving the change: business models and technology. Even as content takes new paths producer to consumer, Adams says, “when you have these 10-year, long-term carriage agreements in place, it’s hard for the [cable TV] industry to respond.”

Deeply ingrained ways of doing business show up even when cable providers or broadcasters try to adapt to the growing presence of OTT. A classic example is HBO Go, which offers on-demand programming over the Internet – but only to existing HBO customers. “They’re trying to adapt, but their business model isn’t changing,” Adams says. Instead, “they are looking to become more competitive with OTT.”

The real potential for OTT may come if it can combine the full-screen ad experience of traditional television with the targeted marketing promised by OTT technologies.

According to Adams, though, that combination is not yet mature enough to attract major advertiser interest and jump start adoption of OTT.

Is Cable Doomed?

“We’ll always be able to choose cable,” analyst Lockett predicts. “It’s in their best interests to appeal to their customer base and they eventually will.”

But even as non-technical people learn more about OTT, Lockett doesn’t see the complete abandonment of cable practices like channel bundling. Unbundling or better bundling won’t be the only thing keeping cable TV alive – instead, cable will have to find a new role. “AM radio is still around after all these years,” Lockett notes, albeit serving a more limited niche.

Adams, too, doesn’t predict the demise of cable. Customers are still dedicated to the big, full-screen watching experience, he believes, and cable remains one of the best ways to get that experience.

Instead, he sees the most revolutionary changes coming TV consumption from the use of tablets and other mobile devices in conjunction with TVs.

A Starring Role for the Second Screen

“The second-screen experience is something the content producers in Hollywood are playing around with now,” Adams explains. “The combination of tablets and TV will change the way we view television forever.”

Tablets and smartphones already provide a range of second-screen experiences – from following Twitter reactions to the Olympic opening ceremonies to show-specific apps like one launched last winter for the popular Fox reality show “American Idol” or the additional show content delivered in the form of a graphic novel for USA Network’s “Burn Notice.”

Meanwhile, companies like Shazam are trying to ease the need for viewers to hunt for apps and content related to a given show. The music-recognition app recognizes the soundtrack from a shows and downloads related content or apps chosen by the show’s producers.

Far from a challenge to cable TV, the second-screen could actually help save it. Cable TV providers could use the second screen to enhance viewing of primary video content and deliver even more targeted advertising – helping to offset income lost from the decline of bundling. That, in turn, would help cable TV service providers hold down subscription costs, and stem the bleeding of customers looking for less expensive alternatives.

Cable TV’s ratings may fall as OTT becomes more popular, but don’t cancel cable’s season just because the plot is getting a major rewrite.